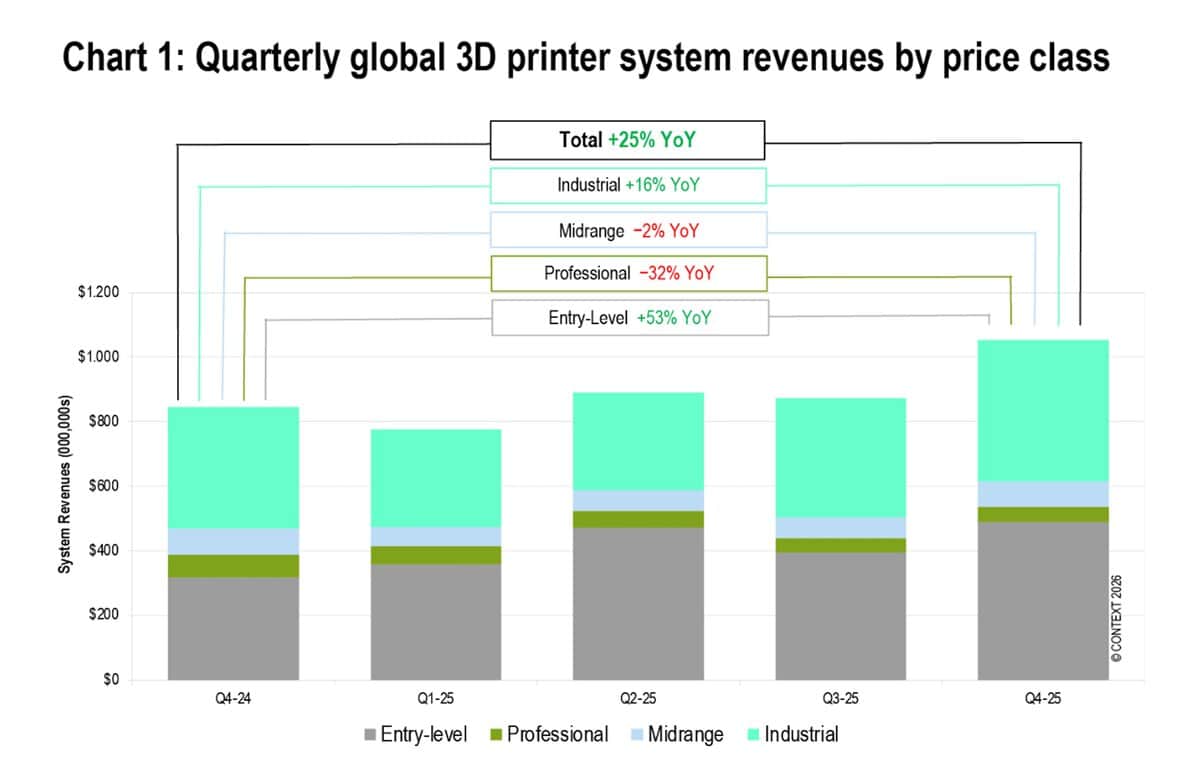

CONTEXT, the global market intelligence firm, has reported that entry-level 3D printers drove a 47% year-on-year shipment surge in Q4 2025, propelling aggregated hardware system revenues up 25% for the quarter. The data, released on April 15, 2026, suggests the global 3D printing industry may have moved past the demand trough that weighed on the high-end market for the previous two years.

The quarter also saw industrial system shipments rebound 12% year-on-year, contributing a 16% rise in revenues, while the entry-level segment alone delivered a 53% increase in revenue. The combined uptick marks a significant turning point for an industry that, as recently as Q2 2025, exhibited sharply divergent performance across market segments, with entry-level growth offset by industrial decline.

Entry-Level 3D Printers Lead Shipments

Entry-level 3D printers (systems priced below US $2,500) shipped to a broad base of consumers, prosumers, professionals, and manufacturing print farms, with volumes rising 26% for the full year 2025. Chinese vendors accounted for over 90% of global shipments in 2025, drawing comparisons to Japan’s dominance in consumer electronics during the 1980s. Almost all technical and price innovation in the segment currently originates from China.

Bambu Lab held a 37% market share in the period, with Creality, Elegoo, and Anycubic also holding top positions. The segment is maturing financially; Creality is on the cusp of an IPO, and multi-billion-dollar investments into other leading vendors by Chinese financial heavyweights have been reported. Innovations in multi-colour 3D printing remain a strong catalyst, as evidenced by Snapmaker’s record-breaking crowdfunding effort.

“Entry-level 3D printing has never been hotter. Nowhere was this more evident than at the recent TCT Asia show in Shanghai, which again showcased ongoing technical innovation and frenetic consumer excitement.”

— Chris Connery, VP of Global Analysis at CONTEXT

Industrial Polymer and Metal Recovery

Global shipments of industrial price-class systems (above US $100,000) rose 12% year-on-year in Q4 2025, continuing a recovery that began in the second half of the year. While full-year 2025 unit volumes were down 3%, the fourth consecutive year of declines, the quarterly rebound extended across both polymer and metal technologies.

Industrial polymer 3D printer shipments grew 23% in the quarter, driven by a 39% surge in Vat Photopolymerisation systems, primarily from a resurgent Carbon and market leader UnionTech. Industrial metal system shipments rose 5%, driven entirely by Metal Powder Bed Fusion (PBF), which grew 24% year-on-year. Chinese vendors BLT, Eplus3D, ZRapid Tech, and Farsoon led in unit share, while Western vendors EOS and Nikon SLM Solutions maintained leadership in system revenue share.

Professional and Midrange Segments Pressured

Both the Professional (US $2,500–US $20,000) and Midrange (US $20,000–US $100,000) segments continued to feel what CONTEXT terms the “Bambu effect,” as demand for Material Extrusion shifted toward entry-level 3D printers at lower price points. Professional segment shipments contracted 12% in Q4 and 15% for the full year, largely due to declining Material Extrusion volumes. Formlabs led the category with 38% market share for the full year, with Vat Photopolymerisation now representing 71% of professional products shipped globally.

Midrange shipments fell 6% in Q4 and 12% for the full year, though Midrange Powder Bed Fusion grew through HP’s upgrade strategy. Market consolidation (mergers, acquisitions, and vendor exits) further distorted year-on-year comparisons in this price class.

Market Growth Outlook for 2026

All key price segments are positioned for growth in 2026, supported by loosening US interest rates, continued strength in China’s domestic market, and sustained aerospace and defence demand globally. Entry-level 3D printers are on track to see the highest growth rate, while industrial shipments are expected to approach double-digit year-on-year increases.

New technology introductions (including composites and full-colour material jetting) are expected to help the Professional segment return to shipment growth. Forthcoming innovations in AI-powered 3D printing, aimed at simplifying at-home printing, also represent a potential catalyst for further market expansion.

The long-term trajectory remains favourable as additive manufacturing progresses beyond prototyping into volume production, with the entry-level 3D printer market increasingly functioning as the industry’s primary financial engine.

About Manufactur3D Magazine: Manufactur3D is an online magazine on 3D Printing. Visit our Global News page for more updates on Global 3D Printing News. To stay up-to-date about the latest happenings in the 3D printing world, like us on Facebook or follow us on LinkedIn and Twitter. Follow us on Google News.